Before closing on a loan, you must go through income verification, which verifies the source of your funds and helps the reviewer determine if you meet their lending requirements. Landlords also use income verification to ensure you can make monthly rent payments.

Whether you’re a full-time employee or an independent contractor, you need to be prepared for income verification, especially if you plan to buy a home or apply for a personal loan. Review the tips below to ensure accuracy and avoid common pitfalls.

What Is Income Verification?

Income verification is a process that involves confirming the following information:

- How much income you have

- How often you receive income

- Sources of your income

It’s an important part of the screening process for mortgages, personal loans and rental properties, and most people go through it at least once in their lives.

How Does Income Verification Work?

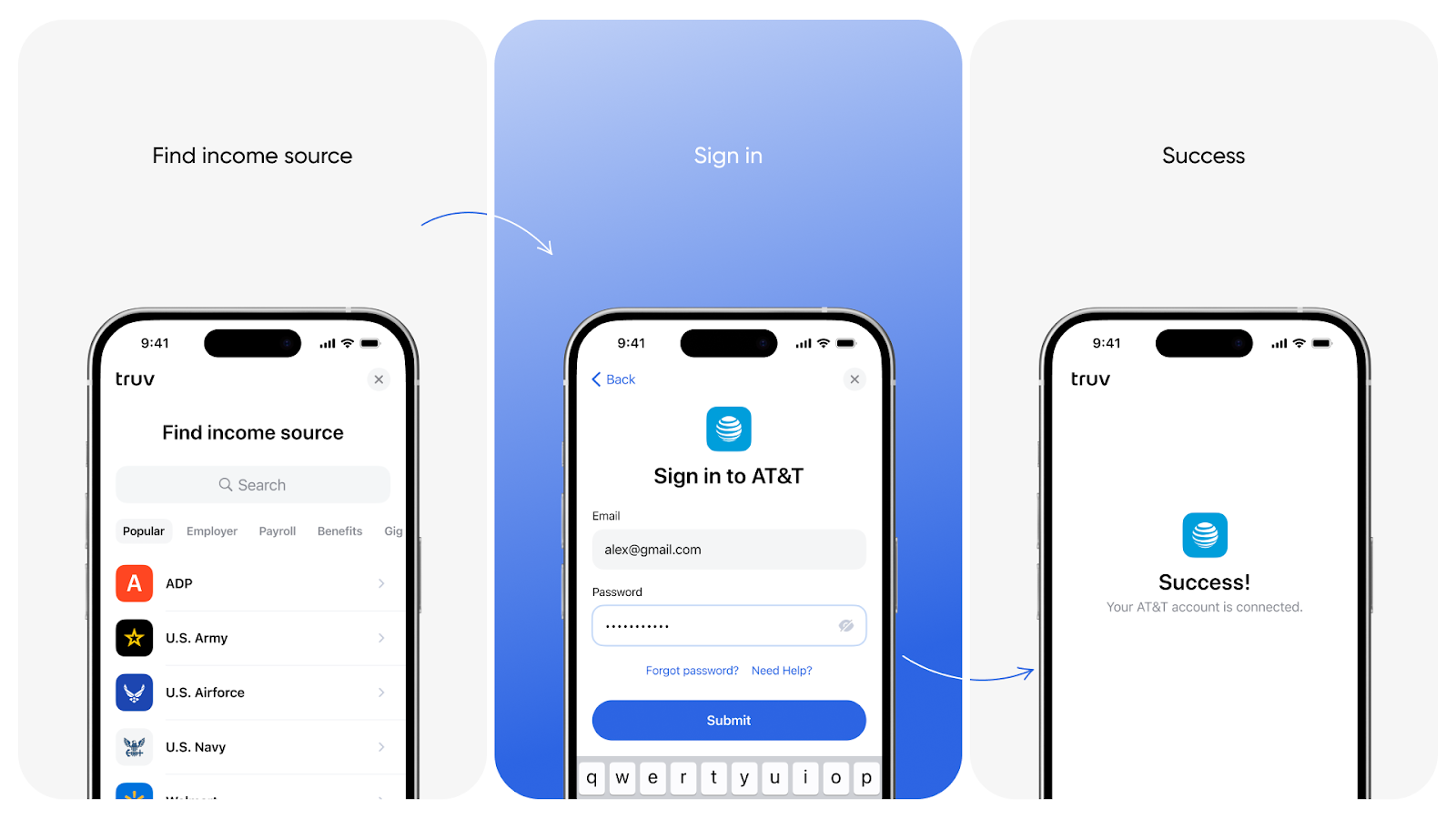

Lenders and landlords use several tools to gather information, such as Verification of Income and Employment (VOIE) databases and consumer-permissioned verification platforms. Consumer-permissioned VOIE provides mortgage lenders with direct access to income and employment details from payroll providers, significantly speeding up the verification process. Instead of the traditional need to gather and upload multiple documents such as paystubs, W-2s, tax returns, or 1099s, lenders can access this information instantly. This not only saves time and effort but also streamlines the lender’s ability to assess your financial situation more quickly and accurately, helping to eliminate delays in the loan approval process.

Some lenders also use manual verification, which involves sending verification forms to each applicant’s employer. An employee representative provides the requested information, and then a loan officer compares the applicant’s information with the completed verification form to ensure everything matches.

In some cases, a lender allows self-attestation with supporting documentation. The self-attestation is a written narrative explaining each income source. Supporting documents include W-2 or 1099 forms, tax returns for previous years and bank statements.

Why Do Lenders Require Income Verification?

Lenders use income verification to protect themselves against fraud, meet legal obligations, and determine the terms for each loan. Occasionally, applicants overstate their income in an attempt to increase their approval odds. Income verification helps identify this type of fraud before approving any loans.

Some lenders offer mortgages backed by government agencies, so they must follow strict approval requirements. For example, the Federal Housing Agency requires lenders to assess the stability of a borrower’s income and document all income sources.

Every loan has an interest rate and a repayment period, which is how long you have to pay back the borrowed money. Lenders use income verification to set these terms. For example, someone with a high income over several years is less likely to default compared to someone with an inconsistent income history. Consequently, the lender might offer the high-income applicant a lower interest rate.

Submitting false income documents is a form of fraud, so always be truthful when going through the verification process. In some cases, providing false information could lead to steep fines or even prison time.

The Common Challenges in Income Verification

Income verification is a necessary process, but there are some challenges, including:

- Mismatch between tax returns and payment documents. Discrepancies beyond outdated forms or typos may require gathering additional information.

- Irregular bonuses and commissions. These can complicate income verification for lenders and landlords. If you’ve changed jobs within two years of applying for a mortgage, keep detailed records to prove your income hasn’t decreased.

- Self-employment difficulties. Freelancers and business owners often lack the standard documents of full-time employees, making verification more challenging. Fluctuating income levels can also make it harder to determine the ability to meet monthly payments.

- Numerous tax deductions. Claiming many deductions on your tax returns can complicate the process, regardless of whether you’re self-employed or work a traditional job.

You can overcome these challenges by maintaining detailed records and keeping copies of tax forms, pay stubs and other income-related documents.

6 Tips for Accurate Income Verification

While income verification processes vary by lender, Truv has seen a significant increase in the adoption of digital and instant verification methods. Consumer-permissioned VOIE, like Truv’s solution, has proven to deliver accurate income and employment information to lenders in under 30 seconds, expediting the underwriting and decision-making process. Whether you’re buying a new home or refinancing, this fast-tracked process can help you close on your home quicker or access your home’s equity faster in the case of a refinance.

As you compare lenders, be sure to inquire about their verification process and ask if consumer-permissioned VOIE is offered. If this efficient method isn’t available, we’ve gathered a list of tips to help you navigate traditional income and employment verification.

1. Salaried Employees

- Have recent salary documents and tax returns available.

- Secure an employment verification letter for your HR department, if applicable.

- Gather documents to help verify any variable income you receive, such as commissions, bonuses and overtime. Every document can be shared automatically with Truv.

2. Self-Employed Individuals

- Keep organized records of all income streams, including freelance work, contract payments and side businesses.

- Track expenses and keep all business-related receipts to ensure accurate reporting of net income.

- Invoice customers at regular intervals to confirm income sources over time.

3. Both Employment Types

- Complete your tax returns on time and ensure they’re accurate, as lenders and landlords are likely to review them during income verification.

- Review and reconcile your bank statements regularly.

- Make sure your bank deposits match your recorded income.

- Review income verification examples to determine the best way to prepare.

4. Seek Professional Advice When Necessary

- Consult with a financial advisor or an accountant to ensure your documents are accurate and comply with legal standards. This is especially helpful for self-employed individuals.

5. Leverage Digital Tools for Income Tracking

- Use a mobile app or an online platform to track income and generate financial reports. A few options include Dime, Spendee and You Need a Budget.

- Look for a tool that integrates with your existing bank accounts for seamless verification.

6. Adhering to Income Documentation Laws

- Familiarize yourself with local, state and federal laws governing income verification. Consult an attorney or a financial professional as needed.

- Keep organized, detailed records in case you’re ever audited by tax authorities or lenders.

- Only share information with trusted entities and ask how they protect sensitive financial data.

See Truv in action and learn how to make income verification easier than ever.

Frequently Asked Questions About Income Verification

What do I need to verify my income?

You need bank statements, previous tax returns, W-2 or 1099 forms, pay stubs and other related documents.

What is the self-employed income statement?

The self-employed income statement, also known as a profit-and-loss statement, summarizes your income and expenses for a given period.

What is your gross income if you are self-employed?

If you’re self-employed, your gross income is the total revenue you earn before deducting expenses.

What is evidence of income?

Evidence of income is a set of documents used to verify your employment and confirm how much money you earn.